A compelling special situation buyout opportunity

Summary:

On July 6th, Sisecam Chemicals Resources proposed a buyout of Sisecam Resources L.P. for $17.90/unit

Last November, Sisecam Chemicals purchased its current stake in the business for an implied price of $33.44/unit

This enormous value discrepancy is unlikely to fly with the Conflicts Committee - the independent board members charged with acting in public unitholders interest

This is one of the most undervalued “initial price” MLP buyout efforts I have seen

Recent MLP buyouts have provided decent bumps to those who purchased prior to a formal offer with very favorable risk/reward

If no deal is made, we are left with a world class asset currently enjoying bullish market conditions while benefiting from a hefty yield - not a bad situation

SIRE situation fits a winning fact pattern

The SIRE situation fits the pattern of recent MLP buyouts that have worked out very favorably for those who purchased after the initial proposal, but before the formal offer.

Year-to-date, I have participated in the BKEP buyout (40% premium to initial price), SRLP (15% premium) and SHLX (23% premium). In addition to the announcement “pop” investors continued to earn a high yield while waiting for the formal buyout announcement.

Each of these situations (among other recent buyouts) created much investor skepticism, yet the outcome was favorable to those who participated as a special situation.

The “MLP buyout” opportunity exists for a few reasons

MLP’s are stranded without much of an investor base

Many investors are scared by memories of being burned by the General Partner

MLP securities have zero (or even negative) utility to their General Partners

Given the above, it makes all the sense in the world for General Partners to buy out their L.P. unitholders

General Partners are more likely to play fair vs. the past

In my view, the successful $690M lawsuit against Boardwalk’s GP cemented a shift in thinking among MLP General Partners who might otherwise be tempted to engage in bad faith acts against their L.P. unitholders.

To date this has held, allowing recent MLP take-privates to trade at levels that created very favorable upside with low risk prior to the formal offer.

Limited float means limited incentive for the GP to “screw” public unitholders

The public float is just 5.1M units vs. 19.8M units outstanding, meaning even a substantial bump in price would require (relatively speaking) only a minor amount of cash outlay relative to SIRE’s intrinsic value and the price the GP already paid just this past November ($33.44/unit).

Two large unitholders (owning a combined ~15% of the float) have already sent letters to the conflicts committee

The first letter can be found here. The second letter was sent from an institutional investor who has not chosen to make their comments public. I encourage all investors in this situation to write a letter to the conflicts committee. They own a decent number of units, which should aid in them seeing things from our point of view:

Business Overview:

Sisecam Wyoming is one of the largest and lowest cost producers of soda ash in the world. Trona, a naturally occurring soft mineral, is processed into soda ash, which is used in a variety of consumer goods, including glass (48%), chemicals (30%), soap (5%), and paper. Soda ash consumption tends to increase in proportion to population and gross domestic product growth rates.

The Green River Basin in Wyoming holds the largest and one of the highest purity known deposits of trona ore in the world. Based upon current production rates and proven and probable reserves reported by Sisecam, the reserve life of Sisecam Wyoming LLC assets is over 50 years.

For the five years prior to covid, SIRE generated $40 to $50M in free cash flow and paid distributions around $2.27 per year. During this time, the unit price traded with a yield of around 7% to 9%, creating a valuation range of between $25 - $30 per unit - far above the current buyout proposal price.

Today’s situation appears far more bullish than the recent past

The following slides were taken from Sisecam’s Chemicals (the GP) presentation after their acquisition of the Ciner L.P. interest last November (since renamed Sisecam Resources, L.P.):

Take your time while studying these slides - they make a powerful strategic case for Sisecam’s L.P.’s assets/business.

In particular, note the low cost advantage that natural soda ash producers have over synthetic producers - particularly in a time of high energy prices. Second, note strong ESG tailwinds for Natural soda ash vs. synthetics.

Even absent a buyout offer (or if it ends up being canceled) SIRE’s business is an outstanding asset that is well positioned for the future

Soda Ash fundamentals appear even more bullish than the above slides suggest

While SIRE has gone quiet on the investor relations front, we are able to get color on industry conditions from Genesis Energy L.P. (GEL) which had their Q2 earnings call on 7/28/2022.

I will quote *extensively* because I think the full comment is worth reading:

“The market for soda ash is structurally short of supply. There's just no other way to describe it or get around that fact. This tightness is fundamentally the result of some 2 million tons a year of supply having been taken offline since 2019. The supply shortage has been exacerbated by multiple production disruptions and force majeure events experienced and declared by other natural producers in the United States over the last 5 or 6 months.

At the same time, the demand is exceeding 2019 levels. This is extremely robust demand, especially considering that the automobile manufacturing business worldwide has been in a recession as a practical matter, having produced millions of fewer cars over each of the last several years, primarily because of the lack of computer chips. This supply shortfall in soda ash means prices must rise to allocate scarce tons and ultimately solicit incremental high-cost synthetic production to balance the market at the margin, all at a time when the synthetic producer’s cost have increased dramatically, owing primarily to rising energy and other input costs.”

“The soda ash market currently finds itself in a spot where worldwide inventories are approaching historical levels low and have never been so low immediately prior to entering a potential policy-induced cyclical slowdown. By way of example, it has been reported at the end of 2021, Chinese inventory levels were approximately 1.8 million metric tons. And today, they are approaching 300,000 metric tons, which is more than an 80% drop in just 6 months.

This provides, in part, the answer to the question of how has China's rolling shutdowns to manage COVID affected soda ash demand and supply dynamics within China. It's fairly obvious to us the net negative effect has been on the supply side of the equation, meaning even fewer tons to potentially seek markets outside of China. All of this has contributed to the fact that our contracted soda ash prices for the third quarter of 2022 will be higher than those in the second quarter.

And this is in a macro environment where technically at least the EU and the United States may be or already are in a recession. We fully expect the structural tightness in corresponding high price environment to continue to exist. In large part, independent of changes in broader economic conditions as we discuss price redetermination for our non-contracted sales volumes in 2023 later this year.

We spent a lot of time analyzing the last 15 to 20 years of soda ash supply and demand. The primary difference between what we are experiencing now and what we experienced in previous economic slowdowns, including the Great Recession of 2008 and 2009 and the pandemic in 2020, was that heading into those economic cycles, the soda ash market was very well supplied. And thus, any significant reduction in demand triggered a corresponding and somewhat immediate price response, albeit short term.

As we pointed out above, market conditions today reflect a very different story with a market that is structurally short of supply. Just as the world is experiencing in the crude oil market, there just isn't any real meaningful incremental supply sitting on the sidelines, just waiting to be turned on and drive prices lower. We believe any pullback in demand would only help further balance the market and not cause any significant downward pressure on prices.”

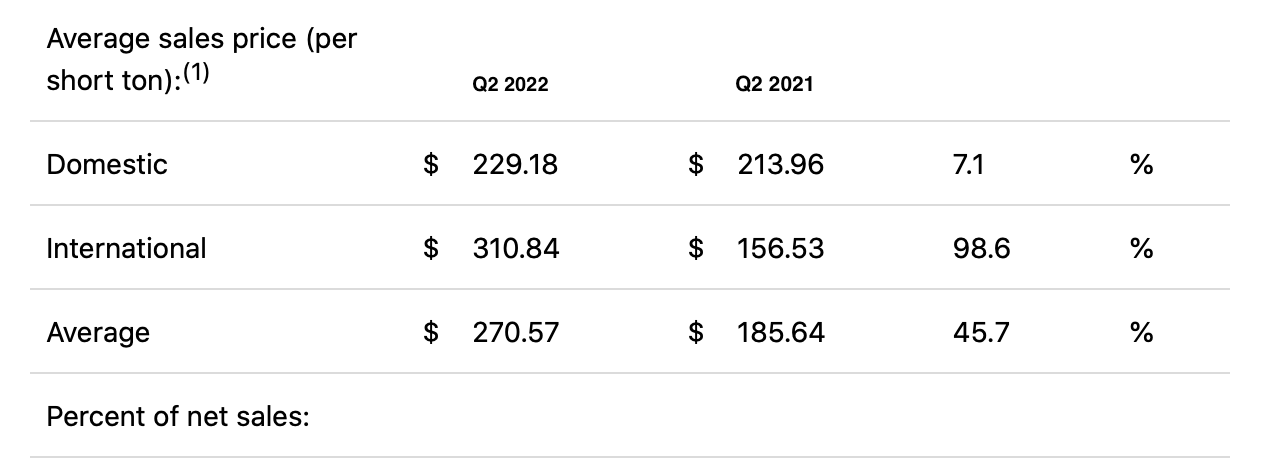

SIRE’s second quarter results were outstanding

The press release can be found here. Pricing confirms the bull case outlined by Sisecam Chemical’s presentation and in the Genesis Energy L.P. Q2 Call, and distribution coverage was 1.6X, which is phenomenal for an MLP.

Base case upside

Sisecam Chemicals acquired their stake last November, when fundamental market conditions were not as favorable. If anything, the underlying business is worth more today.

However, I think we can use what the General Partner paid ($33.44/unit) as part of a base case. if we subtract $2 for the value of the incentive distribution rights (which is generous given, where they are in the payout schedule) we are left with $31.44/unit.

So what discount to this would be reasonable? If we account for the MLP structure/issues, an additional 15% seems plausible (note, i didn’t say fair). This would leave a price of $26.72/unit, plus the likely $1/unit in distributions for a total of $27.72.

This base case would create 29% upside from today’s $21.50 unit price.

When I look at a fair value objectively, I see $36/unit as far closer to a realistic valuation. I get this by putting a 12X multiple on run-rate free cash flow. This is cheap for a world-class asset with long-term fundamental tailwinds.

Of course, the actual outcome will depend on how well the Conflicts Committee advocates for unitholders, which cannot be fully predicted.

The point is not to predict the future with a precise valuation, but to point out that far better outcomes are highly possible.

Framing risk/reward

Given the above, I think SIRE can be safely purchased at a premium to the proposal price of $17.90/unit - I see the probability that this price “holds” as being very unlikely.

A more probable downside case would be a “weak” bump of say 20% - in other words, a price still far below the intrinsic value of the business and absurdly below the $33.44 the GP paid last year.

In this case, a “breakeven” buy level would be around $22.50/unit, given the unitholders receive $1/unit in distributions prior to close ($17.9 * 1.2 + $1) This price would create 23% upside to the $27.72 buyout base upside, or 38% upside to a “closer to equitable” $30 buyout price. In either case the IRR is very strong for a limited risk, finite time horizon position.

Each investor can play with these numbers to manage their own risk/reward viewpoint

Clearly, it is better to buy lower vs. higher. Using history, we will likely get a formal offer in 3 - 6 months. During this time it is probable we will have numerous dips, etc as the security reacts to typical market volatility. (I was able to buy dips in SRLP and SHLX within a month of the final offer, for example). My way of playing this type of situation is to buy a core position, but to leave substantial room to buy on any subsequent dip.

Regardless, buying assets at substantial discounts to fair value with unappreciated catalysts is usually a smart Idea - at this time, SIRE fits this description.

Disclosure: I/we own SIRE units. All ideas, reports, articles, and all other features of this subscription product are provided for informational and educational purposes. Nothing contained herein is investment advice or should be construed as investment advice. Featured analysis might contain errors or be incomplete. All decisions that you make after reading our articles and reports are 100% your responsibility.

Highly compelling idea. My question is whether one is wise to be selective and analytical about each of these on a case-by-case basis or whether one should just buy them all as a takeover wave hits the whole space.