Anti-ESG value buy: 75% upside

I predict a big cash flow ramp-up in this ignored consumer staple

Enormous regulatory moat that few investors understand - if they have heard of the company at all

Market segment is growing in spite of a declining total market

The company’s volume/pricing strategy is not understood and is primed for a period of substantial profit growth

EBITDA and free cash flow are set to ramp up over the next 12-36 months

Expect a substantial increase in capital return with increased profitability

History of massive dividend payments

Not for ESG-sensitive investors

Vector Group (VGR)

Share price: $11.3

Market cap: $1,730 billion

Cash, securities, investments, real estate: $611 million

Debt: $1,384 billion

Net debt: $774 million

Enterprise value: 2,504 billion

TTM EBITDA: $352 million

EV/EBITDA: 7.12X

Debt/EBITDA: 3.9

Net debt/EBITDA: 2.2

Vector Group (VGR) is a manufacturer of deep discount cigarettes. VGR also owns New Valley LLC, which holds minority investments in various real estate projects throughout the United States. The New Valley segment is not material to the investment case, so it will be ignored in this article.

The tobacco segment operates through two subsidiaries, Liggett and Vector Tobacco. For the year ended December 31, 2022, Liggett was the fourth-largest manufacturer of cigarettes in the United States in terms of unit sales. Liggett and Vector Tobacco have no international operations.

Second Quarter results disappointed the market:

What sent the stock careening lower:

Consolidated revenue was down 5.6%, tobacco revenues was down 2.3%

Operating income was down 21%

Adjusted EBITDA down 1.1%

While this doesn’t look good, I believe that the above statistics are not reflective of the future.

What made this quarter look bad

In Q2 2022, VGR had $16 million of real estate revenue and $8.7 million in real estate operating income, vs. 0 in Q2 2023. This 2022 income was related to a property sale. There will be sporadic sales in the future, but this is not a core part of the business.

Q2 2023 contained an unusual $18 million litigation settlement related to a long-standing dispute with the state of Mississippi. As a tobacco company there is potential for additional adverse settlements, but they will be sporadic and are not part of regular operating results.

In my view litigation risk is accounted for by the low valuation multiples of cigarette-related stocks in general. Tobacco EBITDA adjusted for this irregular expense was $94.7 million, up 5.3% relative to the prior year period.

Vector’s deep discount niche

The U.S. cigarette market consists of premium cigarettes, which are generally marketed under well-recognized brand names at higher retail prices, and discount cigarettes, which are marketed at lower retail prices to smokers who are more value conscious.

Since 2004, Liggett has only produced discount cigarettes. According to data from Management Science Associates, Inc., the discount segment represented 29.4% of the total U.S. cigarette market in 2022 compared to 28.3% in 2021 and 28.6% in 2020. Liggett’s domestic shipments of approximately 10.4 billion cigarettes during 2022 accounted for 5.4% of the total cigarettes shipped in the United States during that year.

Vector Group’s massive regulatory moat

Few investors know that VGR has an enormous regulatory moat that allows it to be the lowest cost seller of cigarettes in the United States.

The first 1.93% of VGR’s market share (combining the Liggett and Vector segment exemptions) is exempt from the tax and fee provisions of the Master Settlement Agreement (MSA).

The MSA is the enormous regulatory/tax settlement that the US Government made with the tobacco industry in the late 1990’s. The MSA effectively structured the industry into a cartel, with most of the economic profit going to the state.

You can read about how VGR’s unique MSA exemption came to be in this research paper (If you like business strategy and history, don’t skip this - it’s fascinating).

Essentially, Vector (then called Brooke Group) “cut ranks” with other tobacco companies and decided to work with the US Government. As a reward for this assistance, the US government granted the company a perpetual advantage.

Consistent cash flow growth

Notice that EBITDA (blue bars, above) has dipped slightly in recent years. This is a result of VGR’s deliberate price/volume strategy. I expect EBITDA to rocket higher in coming years.

Before we continue, a little thought experiment - imagine this cash flow growth track record was in any industry other than tobacco, and that like tobacco capital expenditures were minimal. What EV/EBITDA multiple would the stock trade at?

VGR’s price/volume strategy

It is important to understand Vector’s long-term pricing and volume strategy. This strategy deliberately creates a cyclical pattern in results that few investors are aware of.

The strategy starts when VGR introduces a new “ultra deep discount” brand as a competitor to its existing brands and other tobacco products. This brand is radically lower in price than the competition and as such is rapidly adopted by discount-segment tobacco consumers. During this period, VGR expands volumes and takes market share, while margins decline.

When the company is satisfied with volume growth, they shift to a margin growth (price increase) strategy. Their finding is that after building market share and volume at the lower price, consumers tend to stick with the brand through subsequent price increases.

During this phase of the strategy, margins expand and volumes level off or decline. This margin expansion period tends to create very strong EBITDA and net income growth for the company.

Q2 2023 earnings call - excerpts related to the price/volume strategy

“In the second quarter, Liggett's wholesale and retail shipments both outperformed the industry. This outperformance was a driver of the increase in our gross profit of $7.6 million or approximately 7% and which reflects the gradual shift in our strategy on our Montego brand from a volume-based approach to an income-based approach.”

“Our strategy with Montego is consistent with our long-term objective of optimizing profit by effectively managing volume, pricing and market share in our value-based brand portfolio.”

“In the second quarter, we continued to see the benefits of our strategic investment in Montego. After significantly expanding the brand's distribution we have carefully started to increase pricing on the Montego brand at a modest pace… and the price gap between Montego and the industry's leading premium brand remains stable in the range of 45% to 50% discount at retail.”

“Our retail market share gains and profit growth will validate our long-term strategy and competitive advantages in the discount segment. Most importantly, our strategy builds on our foundation for long-term earnings growth.”

Vector’s Tobacco brands

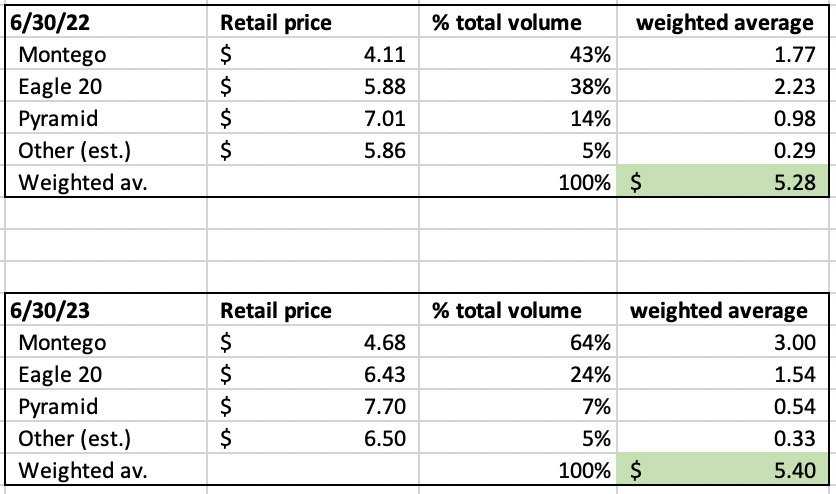

The company at present has three core tobacco brands. The following slide shows the average retail price for each of their cigarette brands.

Note: EDLP means, “everyday low price.” Most of VGR’s volumes are in non-EDLP stores.

As you might have guessed from the above, Montego is the current volume building brand - its discount level is enormous. However, just one year ago Montego’s average retail price per pack was even lower - just $4.11/pack. As can be seen by this 14% year-over-year retail-level price increase, last year Montego entered the margin expansion phase of its development.

“Volume building” brand’s impact on other VGR brands

The promotion of a new “volume building” brand in part cannibalizes the companies existing, higher priced brands. This can be seen below in my estimate of the average selling price per pack of cigarettes across all brands:

As you can see above, Montego grew from 43% in Q2 2022 to 64% of sales in Q2 2023, while higher priced Pyramid fell from 14% of sales to just 7% of sales.

It might be counter-intuitive, but even with the growth of lower-priced deep discount Montego, my estimate is that VGR’s average retail sales price grew 2% year-over-year due to Montego’s 14% price increase.

Volumes skyrocketed in 2022

In December 2021, Korean cigarette company KT&G corp. decided to exit the US market. KT&G is a seller of discount cigarettes that directly compete with VGR’s products. VGR implemented a “full court press” to take this volume by heavily discounting the Montego brand and pushing distribution. This strategy proved successful, as VGR unit volumes increased an astonishing (for cigarettes) 20% in 2022.

The confusing element for many investors is that tobacco EBITDA declined 4% in 2022, suggesting that VGR’s economics were eroding due to a seemingly faulty focus on gaining less profitable volume.

The element missing from this logic is that the margin erosion in 2022 was part of a deliberate strategy - the application of VGR’s long-standing volume/price strategy to the significant opportunity presented by KT&G exiting the market.

VGR’s strategy has now moved into the profit-harvesting mode.

Clarifying Vector’s economics - revenue, per pack economics

Note: Most of the following numbers were created by triangulating information from the 10-Q and other sources such as investor presentations. Some figures contain estimates.

Vector sold about 2.509 billion cigarettes in Q2 2023, which equates to 125.495 million packs of cigarettes.

This implies that VGR made $2.91/pack of GAAP revenue in Q2 2023 (tobacco revenue/pack volume, or 365.6/125.395).

The same computation using Q2 2022 data gets $2.73/pack. The 6.2% increase between our 2023 and 2022 figures ties off with the 6.2% increase in average pricing mentioned in the Q2 2023 earnings call, which seems to validate our figures.

In my view, this GAAP figure inflates true economic revenue and understates VGR’s actual year-over-year price increase.

This is because GAAP revenue includes the excise tax, which is offset by the same tax being included in the cost of goods sold (COGS).

If we remove this tax, VGR’s per-pack revenue was $1.90 in Q2 2023, and $1.72 in Q2 2022. Looking only at this adjusted revenue, average revenue per pack increased by 10% year-over-year.

I estimate that in Q2 of 2024, average retail price per-pack will climb to something around $5.70/pack (a 6% increase yr/yr), with value leader Montego at $5.34/pack.

Q2 2024 - VGR retail price estimates

Note that I kept Montego’s price increase at 14% and reduced the rate of increase for other brands. I also cut the percent of sales of the more profitable Eagle 20 and Pyramid in half.

As this estimated price increase is solely related to VGR’s pricing actions, most or all of this incremental revenue should go to VGR.

Looking only at the portion of revenue that goes to VGR (excluding the excise tax), VGR’s per-pack average revenue will climb to around $2.20/pack from $1.90/pack, a 16% increase.

If we run this experiment for an additional year (maintaining Montego’s rate of price increase, cutting other brands back to a 6% increase, with Montego at 86% of volume) VGR’s average retail price moves up 16% while VGR’s (excluding excise tax) revenue per pack increases 39%.

The point of this thought experiment is not to get precise numbers or estimates. It is to show how retail-level price increases translate into VGR’s incremental per-pack revenue and profitability.

As Montego moves deeper into margin expansion mode, VGR’s per pack “take home” revenue will expand at an increasingly rapid rate.

Volume

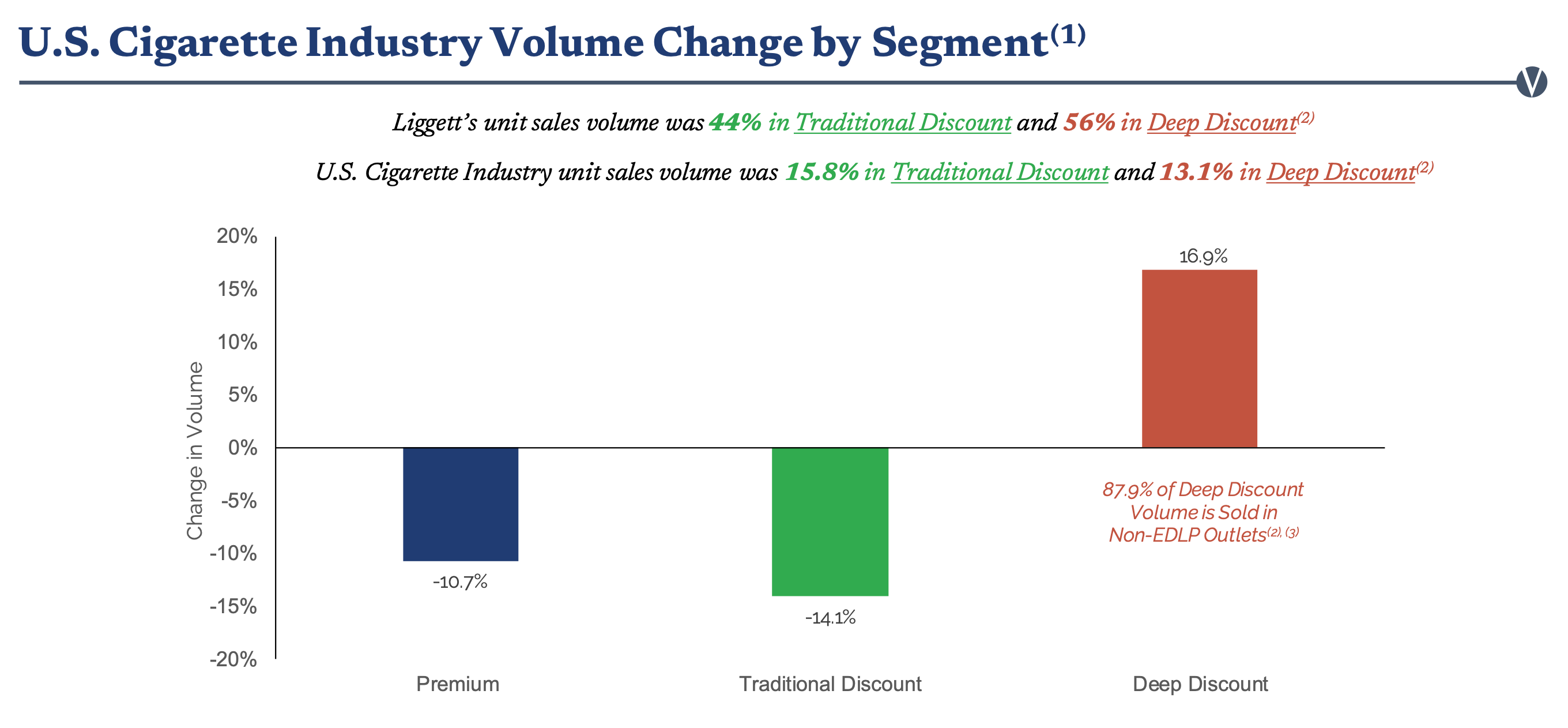

As mentioned earlier, VGR had explosive volume growth in 2022 as it took advantage of KT&G exiting the market. In Q2 2023, VGR’s wholesale volumes were down 8% (vs. -8.9% industry wide) while retail volumes declined 1.8% (vs. -7.1% industry wide).

VGR management believes that retail shipments are a better indicator of industry trends due to inconsistent wholesaler purchasing patterns. In addition, the deep discount segment has been growing in spite of the overall decline in cigarettes.

Post VGR’s 20% volume grab in 2022, I think it is safe to assume that volumes will decline in 2024, particularly given the company’s focus on boosting margins through price increases.

My one year forward estimate of operating income and EBITDA assumes a 4% volume decline, to 121.7 million packs of cigarettes in Q2 2024 (vs. 125.925 million packs in Q2 2023). This is slightly more than the 3.4% volume decline VGR experienced in the first six months of 2023.

If we combine the volume and price estimates I computed above, we get a (excluding the excise tax) revenue figure of $267.5 million. Add the excise tax (which is included in VGR’s top line sales) and GAAP tobacco segment revenue will be around $390.43 million in Q2 2024.

Cost of goods sold

Tobacco is unique in that actual manufacturing and distribution costs are just a small portion of cost of goods sold. The largest portion is various fees and taxes, as seen below:

Excise taxes and MSA expense are related to volume. As can be seen above, even with actual business costs up due to inflation (first two lines) total cost of sales declined year-over-year due to the decline in excise taxes and MSA expense.

Due to the VGR’s MSA exemption on the first 1.93% of market share, incremental volume is (all else equal) lower margin relative to the existing margin. In the same way, a reduction in volume improves margins, as a larger percent of sales is subject to the MSA exemption.

With future price increases significantly boosting per-pack revenue and volume declines cutting into the excise and potentially MSA expense, I think there is room for significant margin expansion over the next 12-36 months.

Potential increase in cash flows - my estimates:

Using my rough estimates, Q2 2024 net income might be around $59 million, up 57% year over year, or 33% relative to an adjusted figure that removes Q2 2023’s unusual items. EBITDA will be around $114 million, creating an annualized or run-rate figure of $456 million - 30% above the current TTM figure of $352 million.

This substantial increase in cash flows will create ample room to increase the regular dividend, issue special dividends, or increase share repurchases.

Directionally accurate

I make no claim that my above estimates will be accurate - in fact, I am certain they are wrong. Margin expansion could be more rapid or slower than I anticipate.

My intent is to illustrate how 2022’s hugely successful “volume boosting” period has set up a period of substantial cash flow growth, as VGR moves deeper into the margin expansion phase of their strategy.

Upside potential

Using an 8X EBITDA multiple (similar to VGR’s multiple prior to the recent share price decline) and my annualized Q2 2024 figure for EBITDA, I get an enterprise value of $3.67 billion, a market cap of 2.9 billion, and a share price of $18.60. Add in 18 months worth of dividends and we get $19.77/share - a 75% total return relative to today’s share price.

The catalyst will be that VGR’s income growth will surprise investors who are not aware of VGR’s cyclical strategy. In addition, I see very strong prospects for increased regular and/or special dividends, as well as share repurchases.

I/we own shares of VGR

Disclaimer

All ideas, reports, articles, and all other features of this subscription product are provided for informational and educational purposes. Nothing contained herein is investment advice or should be construed as investment advice. All decisions that you make after reading our articles and reports are 100% your responsibility.

Our analysis is based on SEC filings, current events, interviews, corporate press releases, and other sources of public information. It may contain errors and you shouldn’t make any investment decision based solely on what you read here. There is no guarantee, or suggestion of a guarantee, that our ideas will perform as they have in the past.

I/my clients or affiliates may hold positions in securities that I write about, which will be disclosed at the time of publication. To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Neither the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss arising, directly or indirectly, from any use of the information contained herein. Nothing presented on this herein constitutes an offer or solicitation to buy or sell any security.