I bought this "GARP" spinoff

Incredible growth track record, market leading brands, +$4B market cap, highly profitable, huge insider ownership - will not stay under-the-radar for long

SharkNinja (SN) is a NYSE-listed spinoff that has to-date recieved very little attention relative to its market-leading brands, incredible growth track record, and $5 billion market cap.

Share price: $36

Diluted share count: 139.3 million

Market cap: $5.0 billion

Net debt: $660 million

Enterprise value: $5,660

2023 EBITDA (EST): $665 million

EV/EBITDA: 8.5X

Net debt/2023 EBITDA: 1X

I don’t think this will be the case for long. Indeed, the company is scheduled to present at the Goldman Sachs retail conference on 9/12, and five sell-side analysts asked questions during the company’s Q2 earnings call (SN’s first such call).

In other words, it looks like there is a clear “awareness” catalyst for what is for-now a massively under-owned growth company.

Odd spinoff creates limited awareness, scant institutional ownership

On 7/31/2023, SharkNinja (NYSE listed) was spun off from JS Global, a Hong Kong listed maker of appliances.

Investors recieved one share of SN for each 25 shares of JS Global. I believe this odd spinoff situation (a Hong Kong listed business spinning off an NYSE-listed company) has resulted in the shares slipping between the cracks.

While (to reporter Andrew Bary’s credit) there was an 8/25 article on the stock in Barron’s, the company has recieved little attention beyond this. Humorously, the only non-spam comment I found under the ticker ($SN) on Twitter suggested that the Barron’s article was a contrarian indicator.

SharkNinja:

SharkNinja is a diversified, global product design and technology company that creates 5-star rated lifestyle solutions through innovative products for consumers around the world.

The Company seeks to leverage its global, agile and cross-functional engineering know-how, product development and manufacturing expertise along with solutions-driven marketing to increase the efficiency, convenience and enjoyment of consumers’ daily tasks and improve everyday lives.

Powered by two trusted, global brands, Shark and Ninja, the Company has a proven track record of bringing disruptive products to market, and developing one consumer solution after another has allowed SharkNinja to enter multiple product categories, driving significant growth and market share gains.

History

SharkNinja (originally known as Euro-Pro Operating LLC) was founded in 1994 by Mark Rosenzweig in Montreal, Canada. Mark’s family had been in the appliance business for years, and Mark initially built upon that success with innovative steam cleaners and upright vacuum designs. In 2003, Mark moved the company to Needham, MA, which is still the company’s global headquarters.

The Shark brand was founded in 2007. Current CEO Mark Barrocas joined the company in 2008, and the Ninja brand was created a short time later.

In 2017, the company was acquired by CDH Private Equity, who structured the acquisition as a subsidiary of JS Global. SharkNinja remained a subsidiary of JS Global until the recent spinoff.

Many of you are likely in the dark on the Shark/Ninja brands

If you are like me (a male with limited experience buying household products) there is a good chance you have never heard of SharkNinja or its two leading brands, Shark (maker of cleaning appliances such as vacuums) and Ninja (food prep, cooking, and beverage appliances).

When I inquired with my wife, I was startled when she delivered her own version of a customer testimonial - we have purchased a number of each brand’s products. She described the brands as, “like Dyson, but at a better price point”.

She mentioned that a colleague had recently replaced all of her kitchen items with Ninja products after having a positive experience with just one item. I was impressed with the way this anecdotal example perfectly matched with the company’s strategy of growing into adjacent product categories via brand reputation.

Shark and Ninja - market leading brands, incredible 20% growth track record

Shark was the number one selling floor care brand in 2022 and Ninja was the number one selling small kitchen appliance brand for the last three years in the U.S. according to NPD (a market research company).

SharkNinja has shown a consistent ability to grow market share in existing categories as well as enter new categories and immediately start taking share:

CEO Mark Barrocas provided these examples in the Q2 2023 earnings call:

In 2021, we entered the ice cream category with the introduction of the Ninja CREAMi which quickly became the number one selling ice cream maker in the U.S., while also doubling the entire category size.

In 2021, we also entered the beauty category with the launch of the Shark HyperAIR Hair Dryers. Within a year, it became the number one selling hair dryer in its price range. This was followed by the successful launch in the fall of last year of FlexStyle, an innovative hair styler and dryer. Year-to-date in 2023, we have a leading market share in hair stylers in the U.S. Additionally, we have also successfully launched FlexStyle in over 17 European countries.

During 2022, we entered the outdoor grill category with the launch of Ninja Woodfire. Building upon our success in indoor cooking, we developed a unique grilling technology, allowing our consumers to deliver authentic woodfire flavors in a sleek and compact product. We have further expanded our presence in outdoor cooking with the recent launch of the Ninja Outdoor Oven.

Just this month, we entered the fast- growing beverage category with our newest innovation, the Ninja Thirsti Drink System. With Thirsti, can personalize and create thousands of drink variations with numerous combinations of flavor, flavor strengths, fizz levels, and sizes at the touch of a button. Through consumer research, we identified the challenges of many households to find better drink options without having to buy a shopping cart full of drinks.

These are just a few examples that demonstrate that solving consumer problems and pain points is at the center of our strategy across every category which we operate.

Since 2008 (when the current CEO was hired) net sales have grown at a compound growth rate of 20%.

CEO Barrocas:

We are not an overnight success. I have been leading SharkNinja’s day-to-day business since 2008, and have been surrounded by an incredible team that has driven the Company’s transformation from an early stage pioneer in small household appliances to a leading global product design company. We have grown our net sales from less than $250 million in 2008 to over $3.7 billion in 2022, a compound annual growth rate of 20% over the last 15 years. We have delivered growth in 14 out of these 15 years, and this growth has been organic. We have not bought a dollar of growth over that period.

December 29, 2014 Forbes Magazine:

Chief executive Mark Rosenzweig, the third generation of his family to lead the company, kick-started the growth by moving the privately-owned company’s headquarters from Montreal, Canada to Newton, Massachusetts back in 2003.

Five years later, the firm radically overhauled its product portfolio, dumping what Rosenzweig referred to as “opening price products” and replacing them with a focus on innovation. Design was moved in-house from external contractors, sharp new brands were created and work began on creating a loyal consumer base.

Sales responded accordingly but Rosenzweig and Euro-Pro president Mark Barrocas wanted the firm to commit to near and long-term “breakthrough goals” in revenue, profit, and customer satisfaction that they believed would require a significant shift in its culture and talent development.

While this excerpt is clearly from a puff-piece article, it manages to provide useful history and insight into how the company’s mission and culture have evolved over time.

The company defines its addressable market as $100 billion - if this is close to correct, there is still an enormous amount of green space for continued growth. For example, if the company is able to grow net sales at just half of the historical rate, they would reach nearly $10 billion in revenue by year 10 - still just 10% of the current addressable market.

SharkNinja’s strategy is defined by three pillars:

Drive growth in existing categories by continuing to innovate and take market share

Expanding across new subcategories and adjacent categories which drives more use-cases and products per household

Build out SharkNinja presence in international growth markets, further globalizing the brand’s potential

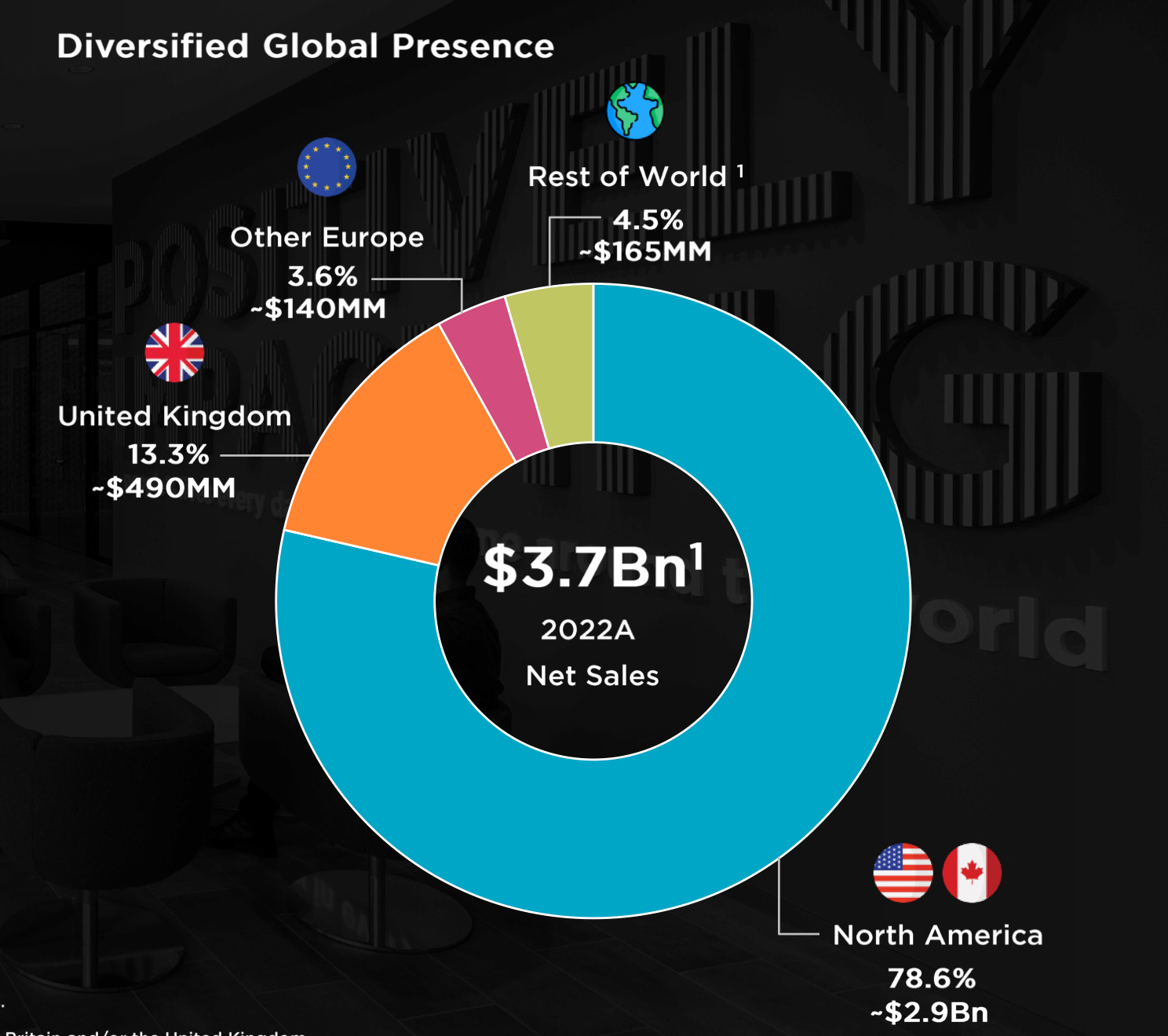

At present, 78% of SharkNinja’s sales are in North America, so the third point (globalization) has substantial promise.

Sales in the UK grew from $50 million in 2014 to nearly $500 million in 2022. The international segment saw 80% growth in Q2, with new markets France and Germany called out as areas of particular opportunity (Q2 earnings call).

A product design and engineering powerhouse

My take-away is that SharkNinja’s strength is a remarkable collaboration between marketing, product design, and engineering. These three strengths are centered around the company’s core mission of solving consumer problems with innovative solutions.

CEO Barrocas describes it this way:

We are a scaled engineering powerhouse where product design is a fundamental part of our culture and our approach to innovation, and design really powers our idea generation machine.

Our global in-house team comprises more than 700 engineer and design associates across Boston, London and China and encompasses the full range of skill sets from R&D, industrial design, mechanical design, mechatronics, electronics, software and IoT. This allows us to have a 24/7 development cycle, enabling ideas to go from sketch to production very quickly.

Our approach to problem solving and designing products is centered around delivering market-leading performance. Multifunctionality, high-quality and extraordinary value to the consumer.

Consumer products deal with everyday tasks, which can be very easy to take for granted and to accept that this is just the way things are done. Our design teams do not accept this, and we pushed to constantly analyze consumers' interactions with small home appliances and leverage consumer reviews to really understand and identify new and unique ways of doing things.

By listening to and testing the consumer at the outset, we aim to develop technologies and systems that are disruptive in the marketplace. Even in subcategories that haven't seen disruptive technology in decades, such as cookware and cutlery, we found a way to bring innovation to the table.

Covid Whipsaw and recovery

Like many consumer product companies, the Covid situation created a 1-2 punch or whipsaw effect in results. Huge demand was followed by massive increases in shipping costs and delays, which was then followed on by across the board cost inflation.

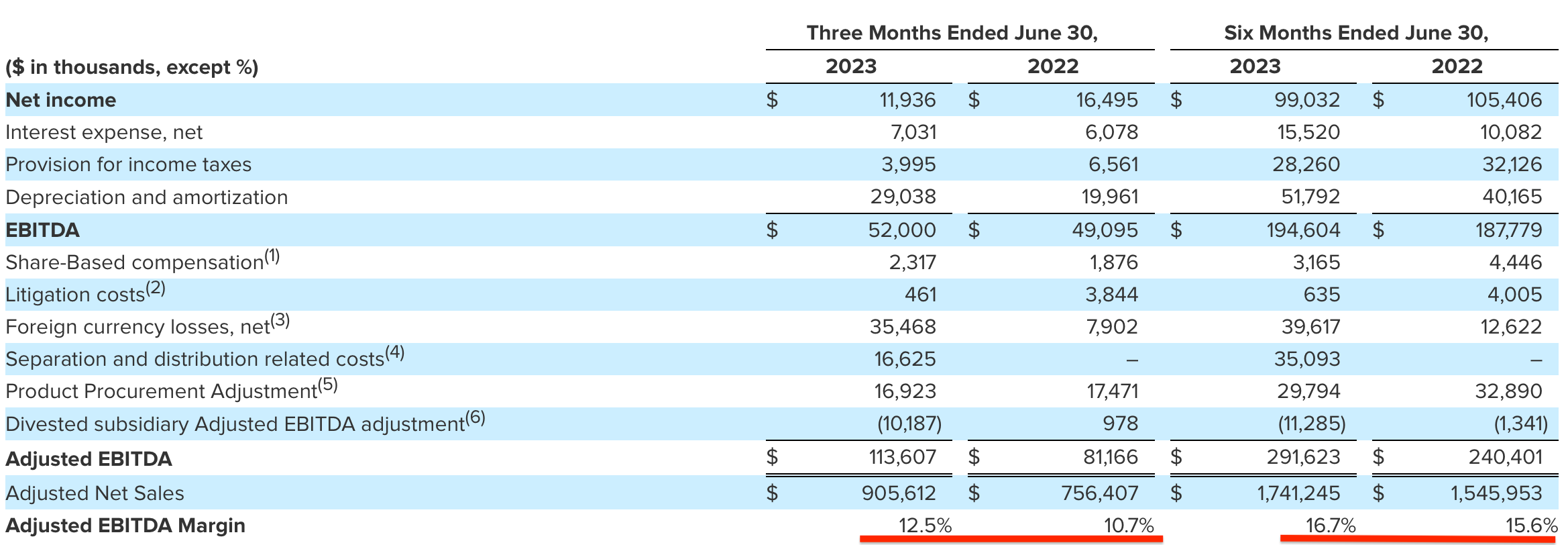

This can be seen in the screenshot below:

Notice that (after 35% growth in 2021) sales flatlined in 2022, while margins compressed.

Q2 2023 showed continued signs of post-covid recovery, with net sales up 22% and continued margin improvement:

In my view, the general pattern of results (the covid boom followed by a hangover) match what has been seen at other consumer-focused companies, while recent results look encouraging.

Company guidance for full-year 2023:

Adjusted Net Sales to increase between 10% and 12%

Adjusted Net Income per diluted share between $2.85 and $3.02, reflecting a 20% to 27% increase vs. the prior year.

Adjusted EBITDA between $650 million and $680 million, a 25% to 31% increase compared to the prior year

Summary

I don’t recall a company with well known, market leading brands, nearly $4 billion in revenue, and a tremendous growth track record coming to market without the fanfare of a typical IPO process.

As a result of this unusual circumstance, SharkNinja looks like a rare case where investors have an opportunity to invest in:

A business with market leading brands, #1 in many categories

A tremendous long-term growth track record - successfully launching innovative products, expanding into new markets, and connecting with consumers

Proven, invested leadership - CEO already engineered revenue growth from $250 million to the current $3.7 billion

A cheap stock - based on guidance for full-year 2023, the company is trading at 12.3 P/E ratio and an EV/EBITDA of 8.5X

Substantial insider ownership - insiders own 58% of shares outstanding

My near-term bull case is for the company to trade between 12X and 15X EV/EBITDA, which would create a share price of between $53 - $67 per share.

The serious upside case will come into play if the company is able to emerge from the Covid hangover and create persistent sales and earnings growth

While there is reason to be confident (it is easy to concoct a wildly higher valuation target assuming a growth rate anywhere close to the historical rate), I am still in the process of assessing SN’s larger potential. Look for future articles on the stock as I further refine my long-term viewpoint.

I/we own SN

Notes:

Disclaimer

All ideas, reports, articles, and all other features of this subscription product are provided for informational and educational purposes. Nothing contained herein is investment advice or should be construed as investment advice. All decisions that you make after reading our articles and reports are 100% your responsibility.

The record of idea performance was computed using data and techniques believed to be accurate. However, it may contain errors and should not be relied upon. It does not represent an investment return. No potential subscriber should view this as a record they can replicate, and actual subscribers should not attempt to do so. Future ideas are unlikely to perform as well as past ideas. Track records of any kind have limited utility.

The service is intended as a source of potential ideas to incorporate into your own process. This newsletter does not provide buy/sell signals and articles should not be interpreted this way.

Our analysis is based on SEC filings, current events, interviews, corporate press releases, and other sources of public information. It may contain errors and you shouldn’t make any investment decision based solely on what you read here. There is no guarantee, or suggestion of a guarantee, that our ideas will perform as they have in the past.

I/my clients or affiliates may hold positions in securities that I write about, which will be disclosed at the time of publication. To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Neither the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss arising, directly or indirectly, from any use of the information contained herein. Nothing presented on this herein constitutes an offer or solicitation to buy or sell any security.