Left For Dead Infrastructure

Huge leverage to operating improvements - Management requested stock instead of cash bonus - Multiple ways to win

I see two ways to win in this stock.

The company has been approached by potential acquirers and an advisor has been hired to review strategic options. A buyout might generate +30% upside from today’s price.

Continuation of their multi-year deleveraging process could potentially generate +200% upside.

Incentives are solid - the majority of the board is independent. Management believes the stock is too cheap and is strongly incentivized to maximize shareholder value.

Key risks: a substantial, prolonged pullback in energy prices, high leverage.

Summit Midstream (SMLP),

…is a value-driven limited partnership focused on developing, owning and operating midstream energy infrastructure assets that are strategically located in unconventional resource basins, primarily shale formations, in the continental United States. SMLP provides natural gas, crude oil and produced water gathering services pursuant to primarily long-term and fee-based gathering and processing agreements with customers and counterparties in six unconventional resource basins

Share price: $17.7

Share count: 10.4 million

Market cap: $183 million

Net debt: $1.359 billion

Pref outstanding: $91 million

Enterprise value: $1.6 billion

2023 EBITDA (EST): $270

Q2-2024 TTM EBITDA (EST) $300 million

EV/EBITDA: 6.6X

Net debt/2023 EBITDA: 5.5X

The most recent presentation can be found here. It provides a solid overview of the asset base as well as management’s strategy.

The bullish setup is simple

SMLP is a highly leveraged system of gathering pipeline assets that is successfully building volumes and cash flow.

Increased EBITDA and debt paydown should bring leverage back in line with peers and allow for the distribution to be turned back on - which if successful will trigger a potentially enormous rally in the stock price.

Management estimates that this deleveraging will occur within 12-24 months. My guess is that ~12 months is too optimistic. I see 18 - 24 months as a more realistic time horizon.

Board of directors has engaged advisors to explore strategic options

A recent press release suggests that there is a second way to win. The company revealed that several parties have approached the company with interest in a 100% buyout. As a result of this interest, SMLP have established a special committee to review strategic options.

Unlike the vast majority of MLP securities, incentives here are strong - there is no inherent conflict of interest. The majority of directors are independent and SMLP itself owns the general partner.

CEO/management is strongly incentivized to maximize shareholder value

Last year, the entire management team opted to replace their cash-based incentive compensation with SMLP “phantom” units.

The above action strongly suggests that the management team believes SMLP units are severely undervalued and that there is upside in the stock.

Why SMLP has been trashed and left for dead

It is easy to see why Summit Midstream Partners has been left for dead by the market.

SMLP is a benighted security type (MLP) that most investors can’t (or won’t) invest in.

MLP securities are expected to pay a yield - SMLP currently pays no distribution.

Like many other MLP securities, SMLP “blew up” legacy investors with enormous losses, leaving the equity trading as a broken stub security.

The story was typical of MLP securities at that time. Prior SMLP management built out their asset base at the top of the market, then the expected volumes failed to materialize. They overbuilt ahead of demand that was too-slow in coming.

The market cap has fallen below $200 million and the stock has little semblance of institutional support or ownership.

The company is over-leveraged and the equity is risky relative to a public peer group.

Last, there is a perception that SMLP’s assets are less desirable and in “tier two” basins (this is accurate, but I think there is more to the story).

In spite of (or perhaps in part because of) the above, I think SMLP is a severely mis-priced asset with substantial upside potential.

Addressing asset quality

Management’s response to my question:

“We believe we have a very strong asset base in great basins with 10+ years of inventory in most basins. While some of our assets might not be in the “core” of most basins, the bright side is the “core” or tier 1 acreage is rapidly running out in most basins (I.e. Williston, DJ, Utica) and activity is moving to tier 2 locations, where Summit is well positioned. I would also mention that the tier 2 acreage is still highly economic at these commodity prices. Additionally, to your Double E point, we do think the market is completely missing the value Double E could bring to SMLP unit holders, mostly due to the org structure and non-recourse asset-level financing we have downstairs at the asset.”

I called around to a number of industry executives who are familiar with these basins. My limited survey provided evidence that the above statement from the company is roughly accurate.

Summit’s historical problem is that their systems were built too far ahead of demand. However, with time and continuing advancement in extraction methods, that issue is working itself out.

With substantial slack capacity, there is now potential to grow cash flows with limited additional capital expenditures.

Immediate catalyst

While I have followed SMLP for a few years, the immediate catalyst that caught my attention was a press release from earlier this month that revealed both strong performance as well as buyout interest from multiple parties.

“Based on the Partnership's recent and expected financial performance, as well as interest recently received from third parties for potential transactions, ranging from the sale of specific assets to consideration for the whole Partnership, SMLP is announcing that its Board of Directors has engaged external advisors to evaluate strategic alternatives for the Partnership with the goal of maximizing value for the Partnership's unitholders.”

The potential sale of individual assets has been an ongoing process that has been disclosed numerous times over the past two years. Indeed, they sold two assets last year. In other words, the only new information here is that the company has received multiple offers for the entire company.

Before we get into the above, I want to review the recent performance mentioned in the above press release:

The company also highlighted volume throughput growth across their various systems:

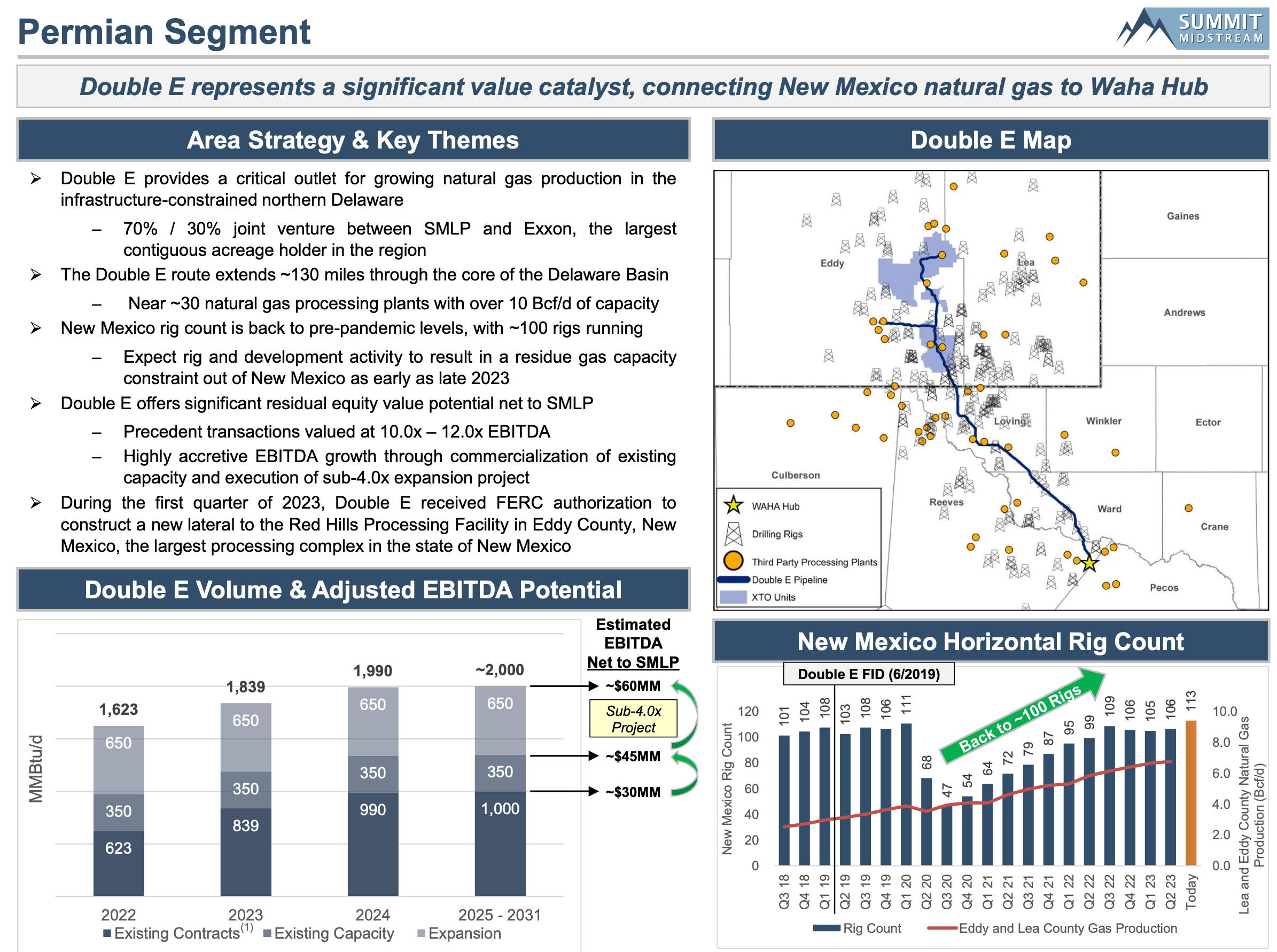

While every system shows substantial growth in volumes, volume growth in the “Double E” system looks particularly impressive.

Double E is a 70% owned joint venture with Exxon that was completed and came on line in November, 2021. I believe 425 MMcf/d is record volume for the pipeline to date.

SMLP management on Double E’s value, Q3 2021 earning call:

Management:

We find it a little interesting, and a kind of scratch our heads just around the value of Double E, and how that's either included or not included in our current market cap. It would appear that the value of that Double E asset is de minimis here, particularly if you think about values, multiples, that other long-haul regulated pipes have commands in the market here recently.

Analysts Question:

And you're pointing out the value… I appreciate it's sort of a long-term asset. Is it something you would consider divesting?

SMLP CFO:

…to your point, if someone comes in and offered the value that we thought was reflective of the equity value of the company, we'd certainly take a look at it. But it's not the base case, but it is something that we would obviously entertain.

It is pretty notable. I mean, when you just look at the EBITDA, and the additional color we provided here, and you do the math on assets like that… the equity value in Double E is probably as much more than what our market cap is today, right?

The market cap of SMLP on 11/4/2021 was around $219 million, so I believe this is a compelling statement of the Double E system’s value.

From the Q3 2023 earnings call:

Analyst:

…then just to shift to Double E. I'm trying to think about how you're thinking about the ramp there from this point. Maybe you can just give us an idea how to think about that.

SMLP CEO:

Yes. Yes, timing is a little hard to predict. But the fundamentals are just continuing to strengthen out there. We know that there's a lot of new plants that have been announced, and they're getting constructed right alongside the Double E footprint. So we still feel very confident that we're going to fill up the pipeline. Right now, we've got about one Bcf a day contracted.

Bill, I believe the ramp has already stepped up, right?

SMLP CFO:

Yes, Gregg. So as we see it, where kind of Eddy and Lea County production sits today, you're right around that kind of wellhead, 2.7, 2.8 Bcf. We think that's a pretty important milestone where volumes kind of north of that should start to migrate towards the pipe.

From Q2 2023 earnings Call:

“…the Permian Basin continues to lead the way in the resurgence of producer activity levels in the U.S., which we believe will drive significant volume growth in the basin and behind our Lane system and the Double E Pipeline. At the current level of rig activity in Eddy and Lea Counties, our projections indicate that existing residue gas takeaway capacity out of New Mexico will become constrained in late 2023 to the early 2024 time frame. And I'm sure many of you are also following the news regarding new pipeline expansions to increase residue gas takeaway from Waha, Texas to the Gulf Coast. Both of these dynamics put Double E in a great position to fill up the remainder of our current 1.35 Bcf a day of capacity over the next couple of years.

SMLP valuation suggests substantial upside potential

The following slide is a good starting point:

If we update the above with the current share price ($17.90), enterprise value is $1.628 billion, and EV/EBITDA is 6.65X. If we give Double E credit for 50% of its value at full (current) capacity, Double E’s equity value to SMLP would be worth $90 million.

My prior research indicated that 8X -9X is a typical multiple for midstream gathering assets, so the peer group SMLP uses appears to be fair.

If we credit SMLP’s fair value at a mid-point multiple of 7.5X (between current value and the peer group) the consolidated assets are worth $37/share. If we add to this our $90 million value for Double E ($8.65/share) the total value per share is $45.65.

I think the above is a conservative estimate of SMLP’s fair asset value. A more aggressive target would use management’s “first half” EBITDA target of $300 million TTM EBITDA, a more aggressive multiple, and a higher value for the Double E system.

For example, if we assume that $270 million of this $300 million target is from the consolidated systems and use an 8.5X multiple, the consolidated business’s equity alone would be worth $832 million, or $80 per share, before any credit is given for the Double E system.

As can be seen, relatively minor tweaks to assumptions can lead to substantial changes in NAV or fair value. This is a result of SMLP’s very low equity valuation and leverage.

To get to the higher targets, I believe the company will need to further deleverage and reinstate a distribution. In my view this process is likely to take 18 - 24 months, assuming no asset sales accelerate the process.

M&A potential

In my view, a near-term sale of the company would trigger more muted upside from today’s share price. Any offer will likely reference the current share price plus some premium (say, 30%), not fair asset value.

Longer term (with additional deleveraging plus volume/EBITDA growth in the core business as well as Double E) I could see a potential sale at a far higher value, closer to our NAV calculations.

Situation now

My read is that the board of directors has received several offers for the entire business, but that the CEO/Chairman feels the offers were too low (as they reference the depressed stock price plus a premium, not NAV).

The management team believes that SMLP is severely undervalued. They are looking for more than the moderate bump presented by current offers (note, this is my speculation).

How the situation unfolds will play out based on two things

How confident management is in growth prospects over the next 2-3 years

How the refinancing process is going

SMLP has notes maturing in 2025 and 2026 that will need to be refinanced. While interest rates are up substantially, management believes that at the time these will need to be refinanced, SMLP’s credit profile will be better and EBITDA leverage will be lower.

CEO J. Heath Deneke had this to say on the Q2 earnings call:

Question:

…how are you thinking about sort of the refi today of your capital structure? And what's the current thoughts?

SMLP CEO:

…we've got $260 million of unsecured that comes due in April of '25. So we're certainly getting kind of close to that 12-month window where we'd like to execute.

Look, we're looking at a range of alternatives here, one being potentially kind of full recapitalization of the second lien and the unsecured, an option of just doing maybe a stub piece of paper to kind of extend out that $260 million unsecured and just do a little mini deal sometime next year.

But I think from a cadence perspective, Gregg, I think about it as we've got some great momentum here coming in the second half. We want to start proving to the market that this growth is coming and that we've got a really good line of sight to kind of that $300 million of LTM EBITDA.

And then as you think about just cadence of when we'll come out with additional information, in February next year, we'll be -- we'll put out our 10-K with calendar year results and come out with our formal guidance at that time. And I think that would be a pretty good time, Gregg, for us to -- once we get all that information out to the market to then go execute on a refinancing.

The company’s notes are currently trading in the mid 90’s, which suggests the credit situation is better than the equity price suggests:

Conclusion

Many of you know that I had a good run with MLP buyout situations in 2021/2022, which I disclosed on Twitter (BKEP, SIRE, SRLP, SHLX). Those situations were different because while there was decent upside, the downside risk (as I saw it) was extremely low.

I believe this situation is equally attractive in terms of expected value, but more speculative - the potential payoffs and risks are more extreme.

If the “public LBO” process continues, SMLP could have hundreds of percent upside potential. However, there is also substantial risk given the high leverage and execution risk (if/if not volumes and EBITDA continue to build as presently appears likely).

As such, I have taken a smaller initial position. I will look to add moderately on any dips so long as fundamentals stay on course.

I/we own shares of SMLP

Disclaimer

All ideas, reports, articles, and all other features of this subscription product are provided for informational and educational purposes. Nothing contained herein is investment advice or should be construed as investment advice. All decisions that you make after reading our articles and reports are 100% your responsibility.

The record of idea performance was computed using data and techniques believed to be accurate. However, it may contain errors and should not be relied upon. It does not represent an investment return. No potential subscriber should view this as a record they can replicate, and actual subscribers should not attempt to do so. Future ideas are unlikely to perform as well as past ideas. Track records of any kind have limited utility.

The service is intended as a source of potential ideas to incorporate into your own process. This newsletter does not provide buy/sell signals and articles should not be interpreted this way.

Our analysis is based on SEC filings, current events, interviews, corporate press releases, and other sources of public information. It may contain errors and you shouldn’t make any investment decision based solely on what you read here. There is no guarantee, or suggestion of a guarantee, that our ideas will perform as they have in the past.

I/my clients or affiliates may hold positions in securities that I write about, which will be disclosed at the time of publication. To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Neither the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss arising, directly or indirectly, from any use of the information contained herein. Nothing presented on this herein constitutes an offer or solicitation to buy or sell any security.