Mesabi Trust's Dividend is about to Cliff-Dive

And the unit price is likely to follow

Mesabi Trust (MSB) is a publicly traded entity that owns a royalty interest in the Peter Mitchel iron ore mine that is operated by Cleveland Cliffs Northshore facility.

Greater details can be found at the Mesabi’s website.

This is a pass-through yield entity and as such, distributions tend to be extremely important to total return - and the stock’s investor base.

I have followed Mesabi for around 10 years and (as some of you might recall) wrote several articles on the security when I believed it was at opportunistic buy points.

Today, the situation is much changed

Unfortunately, Cleveland Cliffs CEO Lourenco Goncalves has a bone to pick with the Mesabi Trust. He does not like the trust’s royalty structure and (more importantly - thanks to recent acquisitions) has no immediate need for Mesabi’s iron ore.

This is a radical departure from the past, when Northshore (and Mesabi’s ore) was a key asset needed to fulfill customer contracts.

As CEO Goncalves stated in the last Cleveland Cliff’s earnings call:

“…For example, we are now extending the ongoing idle at our Northshore [ swing ] facility to at least April of next year. With the increased use of scrap company-wide in our steelmaking operations made possible by the acquisition of FPT last year. The pellets from Northshore are not needed at this time. Rather than deplete this finite resource for the benefit of the Mesabi Trust and its so-called unitholders, we will keep Northshore idle until we decide otherwise.”

This is much worse than what was originally anticipated based on his earlier comments, as I tweeted here:

A shut down until April will blow a massive hole in MSB’s next three distributions.

This is because Mesabi’s distributions correspond with Cliff’s prior quarter earnings - there is a three month lag. Up until this point, Mesabi unitholders have not been impacted by the shut down. This will change with the next three distributions.

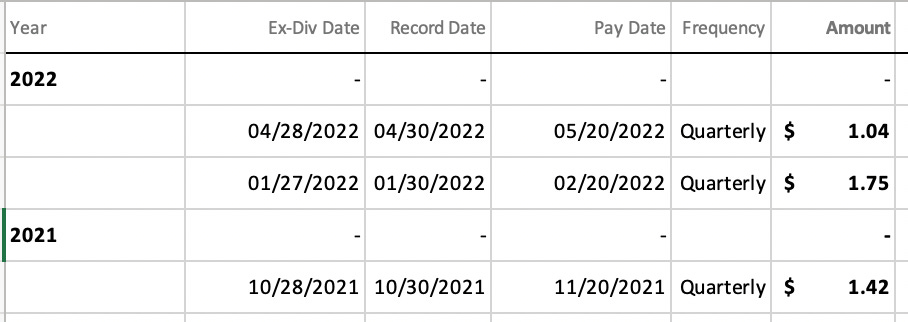

Last year, the distributions for this period were substantial:

Mesabi looks to have north of $10 million in cash reserves after the current distribution is paid (ex date today, July 28th) so the trust itself has resources to weather the storm.

However, it would be prudent for the trustees to pay only minimal (if any) distributions until the production shut-down is resolved.

Why are MSB units holding up so well?

I don’t know, but it does not surprise me. I noticed the borrowing cost to sell short spiked yesterday - suggesting some traders are aware of the issue and starting to act on it.

However, MSB is not the type of stock that most large traders like to short, given its thin volume and the potential for high borrowing costs.

My guess - the stock is holding up due to simple ignorance - the typically wacky trading dynamics in small securities.

Like with many yield securities, most folks look only to the next distribution (which right now, looks good, with the ex date for the last $.84 announced dividend being today, 7/28). As of right now, these folks see zero problems.

There is also the potential that a large institutional unitholder could be supporting the unit price - a specific fund group owns a large % of units outstanding after aggressive purchases over the past several years.

I view this as unlikely.

This fund group tends to take a very long-term view (owning a few of their large positions for ~25 years or so). I would think they would be happy to see the unit price go down (and then at that point, perhaps resume buying).

Bottom line:

Mesabi Trust’s unit price is irrationally high given the coming collapse in distributions and the much degraded situation with Cliffs.

With Mesabi Trust’s ore now used exclusively for internal consumption and alternative sources now available (thanks to Cliff’s recent acquisitions), the leverage the Trust once had with Cliffs has been severely degraded - and I don’t see this fundamental problem getting fixed any time soon.

In my view, Mesabi’s units have at least 50% downside potential from here.

Disclosure: No position at the time of publication. All ideas, reports, articles, and all other features of this subscription product are provided for informational and educational purposes. Nothing contained herein is investment advice or should be construed as investment advice. All decisions that you make after reading our articles and reports are 100% your responsibility.