Sisecam Resources LP $25 offer

Recap of the Sisecam situation, my thoughts now, NATH earnings

Yesterday after the close, Sisecam Resources LP (SIRE) announced that it will be acquired by Sisecam Chemicals for $25/unit.

The deal is expected to close “on or prior to July 30th.” Unitholders are expected to receive distributions until the deal closes, with the next $.50 distribution already announced within the quarterly press release.

The most interesting part of the agreement relative to distributions states (here, page 14):

The Partnership GP has also agreed to declare, and to cause the Partnership to pay, regular quarterly cash distributions to the Partnership’s unitholders during the pendency of the Merger in the amount of available cash for each quarterly period, and to cause such available cash amount to be sufficient to distribute to unitholders an amount equal to or greater than $0.50 per Common Unit (subject to proration for any shorter period in which the closing occurs).

“In the amount of available cash for each quarterly period” and “an amount equal or greater than $.50 per common unit” suggests that they might pay out 100% of “available cash” in any next distributions, with a minimum of $.50/unit.

I am not sure if this is correct, but in my view it does read that way.

If so, this could bump the total consideration, as SIRE has $20M cash on hand plus a very healthy distribution coverage ratio that could fund a larger payout.

Am I content with the acquisition price? Not entirely - I was hoping for closer to $30/unit. However, any low-risk idea that ends with a decent IRR is ok by me.

One curiosity to me is if the reversal of the Boardwalk Pipeline damages impacted the final buyout price.

With the reversal of the above decision, in my view SIRE’s unitholders would have been in a far worse place had the deal broken, given how close the GP (Sisecam Chemicals) is to being able to use the limited call right.

The limited call right is a toxic stipulation in the partnership agreement that allows the GP to force a takeover at the average price of the last 20 days if they own 80% of the units (10-K, p. 44).

This is what occurred in the Boardwalk case. It is a horrible strategic situation for the LP unitholders relative to the GP - in the Boardwalk situation, it allowed the GP to “steal” the units for a truly absurd price.

A counterpoint is the Sprague (SRLP) buyout. It was very similar to SIRE in that the GP was close to being able to use the limited call right, yet unitholders received a moderate bump in price, plus multiple distributions before the deal closed.

If anyone has a view on the potential for a bump, I’d love to hear it.

Trading around a core idea

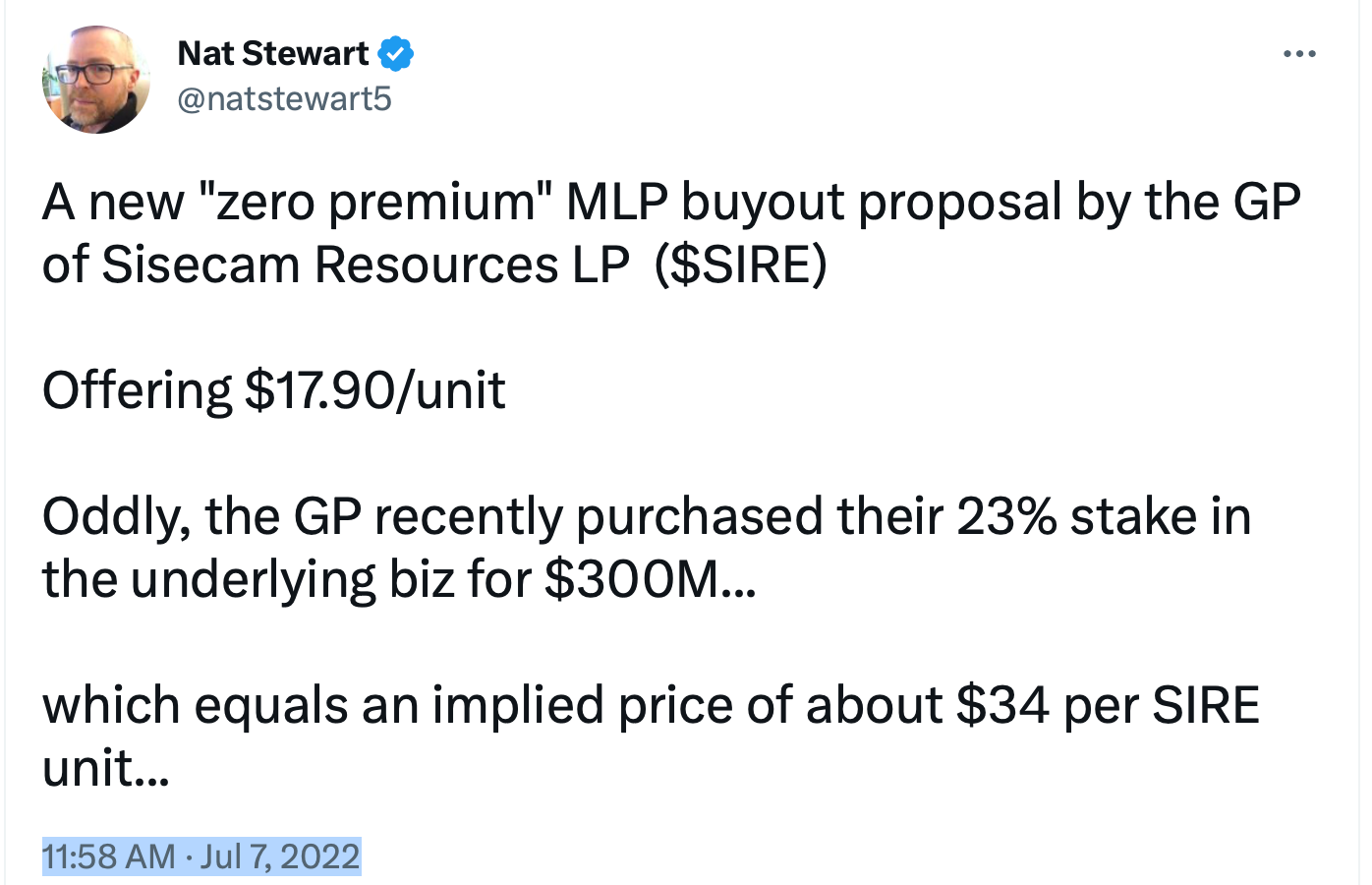

Perhaps the most interesting element of the SIRE idea (and many similar situations) is that there were multiple opportunities to buy the stock relatively close to the initial zero-premium offer - even after the idea was well publicized.

Particularly for smaller or individual traders, this created the opportunity to juice the IRR beyond the “buy and hold” return since the first article’s publication or the initial buyout proposal, which I first commented on here:

(I did that tweet prior to starting this service - new ideas are now published here first)

I purchased units at ~each of these points - it can pay to take ideas you like and implement them opportunistically, taking advantage of market volatility.

Another element (for those who don’t mind making a mess of their MLP taxes!) is that smaller yield securities often have semi-regular trading patterns around their distributions.

For smaller/individual traders, this can help to set up additional potential buy/sell areas that are not open to the big funds - so you can trade within the context of the buyout proposal and potentially boost the final return.

Nathan’s Famous

This morning, Nathan’s Famous just posted EPS +52% year-over-year and boosted their dividend by 11%. This matched my expectation, which I mentioned in the last post. My original feature article on the stock can be found here.

In my view, a floor fair value for NATH is +$100/share. I continue to believe the stock is likely to be added to the Russell 2000 this May during the annual reconstitution, which might boost awareness and trading volume in the stock.

Next article

My next feature article will feature an under-the-radar “GARP” stock that has an enormous reinvestment runway at favorable returns - the classic compounder situation. Importantly, the industry/sector that has a large investor constituency - this stock will not stay under the radar forever. I see several hundred percent upside potential over the next 2-3 years.

I/we are long SIRE, NATH

Disclaimer

All ideas, reports, articles, and all other features of this subscription product are provided for informational and educational purposes. Nothing contained herein is investment advice or should be construed as investment advice. All decisions that you make after reading our articles and reports are 100% your responsibility.

Our analysis is based on SEC filings, current events, interviews, corporate press releases, and other sources of public information. It may contain errors and you shouldn’t make any investment decision based solely on what you read here. There is no guarantee, or suggestion of a guarantee, that our ideas will perform as they have in the past.

I/my clients or affiliates may hold positions in securities that I write about, which will be disclosed at the time of publication. To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Neither the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss arising, directly or indirectly, from any use of the information contained herein. Nothing presented on this herein constitutes an offer or solicitation to buy or sell any security.

A little follow up on NATH related to a question I received. The stock is still cheap in my view relative to it's economic qualities as a public company or its private market value. In the few years pre-covid, it traded with a floor valuation of 12X EV/EBITDA and a ceiling valuation of 18X EV/EBITDA.

Using my fiscal 2023 EBITDA estimate, the pre-covid "floor" multiple of 12X would create a floor price of $95/share. The ceiling value would create a price target of $148/share. 15X mid point could create a share price of $120/share. Given how well the stock performed during covid and the fact they own a leading CPG brand in their space with $320 million or so of system-sales to grocery stores, I don't think the current valuation is reasonable.

A more reasonable trading range would IMO be $95 - $120/share. Given it traded at this level pretty consistently pre-covid, IMO it seems reasonable today - it reverts slowly in part because few want to buy into a lower volume stock - which is why, IMO a possible index inclusion is a potential catalyst to push it back into a fair value range. But we shall see.

Congrats and thank you for the great call. Much appreciate your insights this morning, as (i) the language in the agreement about the distribution is peculiar, and (ii) the reversal of the Boardwalk decision had concerned me. (Regarding the Boardwalk reversal, I can assure you that a corporation can get an opinion from counsel that says almost anything. By way of example, Enron got opinions from V&E and Andrews and Kurth that all its deals were in compliance with law.) As for the sale price, it was done at less than 8x trailing EPS -- when trailing EPS was artificially lower because the company didn't ship 15% of production in the 4Q -- which seems very low in a rising price environment. It would be nice if anyone knows how to contact Justin Evans to see if his family office will be challenging the deal, as was indicated as a possibility in their letter to the board and which you tweeted back in July. https://twitter.com/natstewart5/status/1548728814871744512?lang=ar